Difference between Bookkeeping & Accounting- As we know every individual performs some kind of economic activity in their life. such as a salaried person gets a salary and spends to buy provisions and clothing, for children’s education, construction of a house, etc. A sports club formed by a group of individuals, a business run by an individual or a group of individuals, a local authority like Calcutta Municipal Corporation, Delhi Development Authority, and Governments, either Central or State, all carrying some kind of economic activities.

Not necessarily all economic activities are run for any individual benefit; such economic activities may create a social benefit that is beneficial for the public, at large.

Anyway, such economic activities are performed through ‘transactions and events’. The transaction is used to mean a business, the performance of an act.

Contents of this post

What is Bookkeeping?

Book-keeping is an activity concerned with the recording of financial data relating to business operations in a significant and orderly manner. It covers procedural aspects of accounting work and embraces the record-keeping function. Obviously, book-keeping procedures are governed by the end product, the financial statements. The term ‘financial statements’ means Profit and Loss Account, Balance Sheet, and cash flow statements including Schedules and Notes forming part of Accounts.

What are the features of Bookkeeping?

There are many features in Bookkeeping but the most important features are mentioned below.

First is the complete Record of Financial Transactions.

Collecting and Producing the Source Documents.

Maintaining the Journals, Ledgers, and Subsidiary Books.

Maintaining other source documents and books of accounts.

Recording the financial transactions in Journal.

Posting the recorded transactions to relevant Ledger Accounts in the ledger is called Ledger Posting.

Balancing the Ledger Accounts.

Classifying the accounts as Expense, Income, Asset, and Liability.

Prevention and Detection of Frauds and Errors.

Completing the process of Payroll Accounting.

What is Accounting?

Accounting is the art of recording, classifying, and summarising in a significant manner and in terms of money, transactions, and events which are, in part at least, of a financial character, and interpreting the result thereof.” According to this definition, accounting is simply an art of record keeping. The process of accounting starts by first identifying the events and transactions which are of financial character and then recorded in the books of account.

What are the features of Accounting?

The features of Accounting are given below:

Recording – This is the basic function of accounting. As we know, All business transactions of a financial character, as evidenced by some documents such as sales bills, passbooks, salary slips, etc. are recorded in the books of account. And this recording is done in a book called “Journal.”

Summarising – It is concerned with the preparation and presentation of the classified data in a manner useful to the internal as well as the external users of financial statements. This process leads to the preparation of the financial statements.

Classifying – Classification is concerned with the systematic analysis of the recorded data, with a view to group transactions or entries of one nature in one place so as to put information in compact and usable form. The book containing classified information is called “Ledger”. This book contains on different pages, individual account heads under which, all financial transactions of similar nature are collected. For example, there may be separate account heads for Salaries, Rent, Printing and Stationeries, Advertisement, etc.

Analyzing – The term ‘Analysis’ means a methodical classification of the data given in the financial statements. The figures given in the financial statements will not help anyone unless they are in a simplified form. For example, all items relating to fixed assets are put in one place while all items relating to current assets are put in another place.

Interpreting – This is the final function of accounting. It is concerned with explaining the meaning and significance of the relationship as established by the analysis of accounting data. The recorded financial data is analyzed and interpreted in a manner that will enable the end-users to make a meaningful judgment about the financial condition and profitability of the business operations. The financial statement should explain not only what had happened but also why it happened and what is likely to happen under specified conditions.

Communicating – It is concerned with the transmission of summarised, analyzed, and interpreted information to the end-users to enable them to make rational decisions. This is done through the preparation and distribution of accounting reports, which include besides the usual profit and loss account and the balance sheet, additional information in the form of accounting ratios, graphs, diagrams, fund flow statements, etc.

What is Accountancy?

Accountancy implies the systematic body of knowledge that prescribes accounting principles, conventions, and techniques, which are to be followed during the accounting process. Accountancy is the set of concepts, principles, techniques, and rules that constitutes the framework of accounting. Also, accountancy entails complete knowledge of accounting which includes both conceptual understanding of the subject and practical application to the maintenance of books of accounts.

Accountancy is the practice of recording, classifying, and reporting business transactions for a business. It provides feedback to management regarding the financial performance and financial status of an organization. The practice of accountancy has crossed its usual domain of preparation of financial statements, interpretation of such statements, and audit thereof.

What is the difference between Bookkeeping and Accounting?

The difference between Bookkeeping and Accounting

S.No.

Book-keeping

Accounting

1.

It is a process concerned with the recording of transactions.

It is a process concerned with summarising the recorded transactions.

2.

It constitutes a base for accounting.

It is considered a language of the business.

3.

Financial statements do not form part of this process.

Financial statements are prepared in this process on the basis of book-keeping records.

4.

Managerial decisions cannot be taken with the help of these records.

Management makes decisions on the basis of these records.

5.

There is no sub-field of book-keeping.

It has several sub-fields like financial accounting, management accounting, etc.

6.

The financial position of the business cannot be ascertained through book-keeping records.

The financial position of the business is ascertained on the basis of the accounting reports.

7

Bookkeeping is carried out by junior staff.

Accounting is done by senior staff with the skill of analysis.

What is the difference between Accounting and Accountancy?

The difference between Accounting and Accountancy

S.No

Accounting

Accountancy

1.

Accounting is a systematic process that involves measurement, recording, classification, summarizing, presenting, and interpreting the financial information of an organization.

Accountancy implies the systematic body of knowledge that prescribes accounting principles, conventions, and techniques, which are to be followed during the accounting process.

2.

Nature of work performed by the accountants.

Profession pursued or opted by the accountants.

3.

This is a practical part only

Both theoretical and practical part

4.

It is an action based on the knowledge of accountancy.

It is a field of knowledge that indicates the route to accounting.

5.

Narrow

Wide

6.

Financial Statements

Principles and Techniques

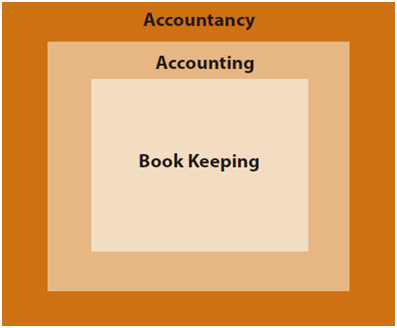

What is the relation between Bookkeeping, Accounting, and Accountancy?

According to the above picture, you can understand that the process of bookkeeping becomes accounting and the full process of accounting comes under Accountancy.

Further Faqs

Who is an Accountant?

An accountant is a professionally qualified person who performs accounting functions, i.e. preparing and maintaining accurate financial records of the enterprise.

What are the objectives of Book-keeping?

Objectives of bookkeeping 1. Complete Recording of Transactions and 2. Ascertainment of Financial Effect on the Business.

What are the various sub-field of accounting?

The various sub-fields of accounting are: (i) Financial Accounting (ii) Management Accounting (iii) Cost Accounting (iv) Social Responsibility Accounting (v) Human Resource Accounting

Who are the users of accounting information?

The various users of accounting information: (i) Investors (ii) Employees (iii) Lenders (iv) Suppliers and Creditors (v) Customers (vi) Government and their agencies (vii) Public (viii) Management

An Accountant, GSTP, GST blogger, Website Creator, SEO Builder & Co-founder of the website https://gstportalindia.in for the help of GST Taxpayers of India. Having a perfect accounting experience of more than 10 years in a Private Ltd Company.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.