CTS full form

CTS full form is Cheque Truncation System. It is the best project of the Reserve bank of India for making the cheque clearance system faster. Today, in this blog post you will learn more unknown facts about the CTS system in banking in India.

CTS stands for –Cheque Truncation System

Contents of this post

What is Cheque Truncation System (CTS)?

The cheque Truncation system is the process in which an electronic image of the cheque is transmitted to the paying branch through the clearing house, along with relevant information such as presenting bank, date of presentation, MICR Band, etc. This process helped very well to stop the flow of the physical cheque issued by a drawer at some point by the presenting bank en route to the paying bank branch. This process also eliminates the cost of movement of the physical cheques, reduces the time required for their collection, and brings smoothness to the entire activity of cheque processing.

How CTS system work?

CTS system works as the transmission of required data through electronic mode. Here are the points that will help to understand how to CTS system works-

- In CTS, the presenting bank (or its branch) captures the data (on the MICR band) and the images of a cheque using their Capture System (comprising of a scanner, core banking, or other application) which is internal to them and meeting the specifications and standards prescribed for data and images under CTS.

- To ensure the security, safety, and non-repudiation of data/images, end-to-end Public Key Infrastructure (PKI) has been implemented in CTS. As part of the requirement, the collecting bank (presenting bank) sends the data and captured images duly signed digitally and encrypted to the central processing location (Clearing House) for onward transmission to the paying bank (destination or drawee bank). For participating in the clearing process under CTS, the presenting and paying banks use either the Clearing House Interface (CHI) or Data Exchange Module (DEM) that enables them to connect and transmit data and images in a secure and safe manner to the Centralised Clearing House (CCH).

- The Clearing House processes the data, arrives at the settlement, and routes the images and requisite data to the paying banks. This is called presentation clearing. The paying banks through their CHI / DEM receive the images and data from the CCH for further processing.

- The paying bank’s CHI / DEM also generates the return file for unpaid instruments, if any. The return file/data sent by the paying banks are processed by the Clearing House in the return clearing session in the same way as presentation clearing and return data is provided to the presenting banks for processing.

- The clearing cycle is treated as complete once the presentation clearing and the associated return-clearing sessions are successfully processed. The entire essence of CTS technology lies in the use of images of cheques (instead of physical cheques) for payment processing.

What are the benefits of CTS in banking?

These are the Benefits for all such as

✔️ Customer Benefit

- Extended cut-off time for acceptance of Customer Cheques by banks

- Easy retrieval of information

- Reduced timelines for clearing

✔️ Operational Benefit

- MICR amount encoding is not required

- Reconciliation difference eliminated – MICR and Image data travel together

- No cheques being lost/tampered/pilfered

- No risk of any manipulation of data and images during transit

- CTS 2010 standards leading to enhanced security and automation

✔️ Commercial Benefit

- The cost involved in paper movement eliminated

- Grid implementation allows better liquidity management for banks

✔️ Fraud Prevention Mechanism Provided

- Manipulation of data and images during transit is prevented by digital signature/encryption.

- CTS 2010 standards lead to enhanced security (Pl refer to attached NPCI circular for CTS 2010 standard) MICR reject repair flag

✔️ Decrease in Time Scales

How CTS worked to decrease time scales?

According to npci.org.in

Prior to CTS clearing, instruments were used to get settled in MICR clearing. There was a total of 66 MICR centers across India. These MICR centers used to undertake clearing & settlement in their local geography. The intra-MICR clearing was considered outstation clearing. During MICR clearing physical instruments were traveling for clearing to respective MICR centers. The typical flow for clearing is explained in the next paragraph.

The customer deposits an instrument in dropbox/ collection point / Bank-Branch. All instruments received before a cut-off time are collected & physically transported to the service branch of the presenting bank. The instruments would get sorted as per MICR clearing centers & would physically travel to the corresponding MICR clearing centers i.e. Local or outstation clearing. At MICR centers respective banks would present and collect their instruments. These would be taken through the same route to the respective bank branch for processing. The rejected instruments would traverse the same route from the bank to presenting bank branch. The return cycle of rejected instruments would be completed the next day & settlement is completed on the completion of the return cycle. The customer would get funds on completion of the settlement process.

In the CTS scenario, the physical instrument is truncated at presenting bank end (either at the branch level or service branch level). The images & data of the collected instruments captured at presenting bank would travel electronically to the drawee bank for processing the same day. The return cycle would be completed the next day. The return cycle would be completed the next day & settlement is completed on the completion of the return cycle. The customer would get funds on completion of the settlement process. Further, all clearing locations are divided into 3 regional grids. All Clearing locations of a grid are settled together on a T+1 basis.

Report on the cheque truncation system operations in 2022

These are the report on the CTS system operations in the last financial year through the source NPCI

Southern Grid CTS – Month-on-Month Volume & Value Report (FY April 2021 to March 2022 )

| Month | Presentment Cheque Volume (in Lakhs) | Presentment Cheque Value (INR Lakhs) | Return Cheque Volume (in Lakhs) | Return Cheque Value (INR Lakhs) | Return Cheques as % of Total Presentment Cheque Volume |

| Apr-21 | 173.80 | 17,439,654.08 | 10.58 | 1,303,596.09 | 6.09% |

| May-21 | 96.95 | 93,986.36 | 5.95 | 7,147.90 | 6.13% |

| Jun-21 | 120.92 | 12385831.05 | 5.74 | 857537.49 | 4.74% |

| Jul-21 | 166.04 | 16,600,094.59 | 8.52 | 1,163,523.28 | 5.13% |

| Aug-21 | 168.38 | 16,387,411.06 | 8.43 | 1,093,259.92 | 5.01% |

| Sep-21 | 179.12 | 17,613,563.64 | 9.36 | 1,313,634.05 | 5.22% |

| Oct-21 | 171.25 | 16,844,238.34 | 10.49 | 1,340,496.81 | 6.13% |

| Nov-21 | 167.64 | 16,529,444.95 | 9.16 | 1,227,179.10 | 5.46% |

| Dec-21 | 188.43 | 18,901,772.46 | 11.96 | 1,540,290.81 | 6.35% |

| Jan-22 | 168.03 | 16,412,250.67 | 9.17 | 1,172,876.59 | 5.45% |

| Feb-22 | 165.93 | 16,885,678.41 | 8.49 | 1,201,033.09 | 5.12% |

| Total | 1,766.50 | 166,093,925.61 | 97.84 | 12,220,575.14 | 5.54% |

Western Grid CTS – Month-on-Month Volume & Value Report (FY April 2021 to March 2022 )

| Month | Presentment Cheque Volume(in Lakhs) | Presentment Cheque Value(INR Lakhs) | Return Cheque Volume(in Lakhs) | Return Cheque Value (INR Lakhs) | Return Cheques as % of Total Presentment Cheque Volume |

| Apr-21 | 226.57 | 22,145,589.34 | 10.76 | 1,268,001.92 | 4.75% |

| May-21 | 94.97 | 96,149.80 | 7.18 | 9,529.06 | 7.56% |

| Jun-21 | 245.52 | 20452840.86 | 8.47 | 1108965.91 | 3.45% |

| Jul-21 | 263.78 | 22,095,921.78 | 10.27 | 1,242,950.07 | 3.89% |

| Aug-21 | 260.77 | 21,610,431.79 | 10.16 | 1,214,983.12 | 3.90% |

| Sep-21 | 268.57 | 22,065,746.11 | 10.43 | 1,300,055.30 | 3.88% |

| Oct-21 | 290.45 | 24,095,187.65 | 11.62 | 1,431,486.18 | 4.00% |

| Nov-21 | 246.52 | 20,648,343.96 | 9.97 | 1,215,799.02 | 4.04% |

| Dec-21 | 288.02 | 25,789,081.48 | 14.06 | 1,762,124.72 | 4.88% |

| Jan-22 | 270.50 | 23,077,194.14 | 11.23 | 1,472,536.39 | 4.15% |

| Feb-22 | 259.53 | 22,586,623.64 | 10.79 | 1,466,060.16 | 4.16% |

| Total | 2,715.18 | 224,663,110.56 | 114.93 | 13,492,491.83 | 4.23% |

Northern Grid CTS – Month-on-Month Volume & Value Report (April 2021 to March 2022)

| Month | Presentment Cheque Volume(in Lakhs) | Presentment Cheque Value(INR Lakhs) | Return Cheque Volume(in Lakhs) | Return Cheque Value (INR Lakhs) | Return Cheques as % of Total Presentment Cheque Volume |

| Apr-21 | 157.44 | 15,750,505.83 | 13.64 | 1,647,139.92 | 8.67% |

| May-21 | 175.62 | 152,877.19 | 6.65 | 8,891.16 | 3.78% |

| Jun-21 | 144.94 | 14904350.92 | 8.28 | 1399007.87 | 5.72% |

| Jul-21 | 166.32 | 16,629,644.55 | 10.69 | 1,599,887.22 | 6.43% |

| Aug-21 | 159.45 | 15,392,432.49 | 9.82 | 1,436,168.20 | 6.16% |

| Sep-21 | 176.43 | 16,967,498.36 | 10.99 | 1,603,676.79 | 6.23% |

| Oct-21 | 173.49 | 17,320,982.30 | 11.95 | 1,655,822.82 | 6.89% |

| Nov-21 | 162.84 | 16,144,535.66 | 10.32 | 1,480,199.84 | 6.34% |

| Dec-21 | 183.87 | 19,400,737.79 | 14.41 | 1,990,997.54 | 7.84% |

| Jan-22 | 158.47 | 16,282,713.38 | 10.76 | 1,607,068.60 | 6.79% |

| Feb-22 | 156.53 | 16,066,568.56 | 9.92 | 1,624,848.98 | 6.34% |

| Total | 1,815.41 | 165,012,847.03 | 117.44 | 16,053,708.93 | 6.47% |

What is a CTS cheque?

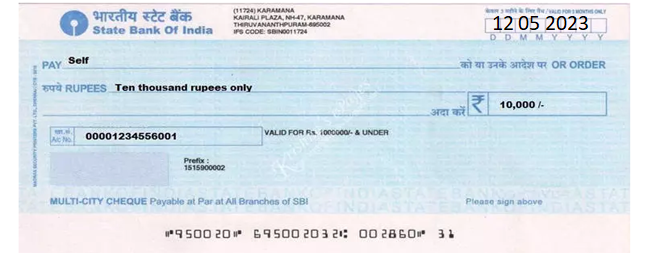

CTS cheque means a cheque on which the printer’s name with CTS-2010 was written across the left side of the cheque. This cheque can be cleared through the cheque truncation system after depositing that cheque into the bank branch for clearing.

What is the format of the CTS cheque?

CTS cheques have all these types of information-

- Branch address along with bank IFSC on top of a cheque.

- Date in dd/mm/yy format in boxes.

- The printer’s name with CTS-2010 was written across the left side of the cheque.

- A pantograph is placed below the account number, which will show “Void/Copy” if someone takes a photocopy of the cheque.

- Rupee symbol.

- The words “Please sign above” are written on the bottom of the cheque.

- The visible watermark “CTS India” (to be visible if the cheque is placed in light).

- The ultraviolet logo of the Bank is to be printed at the upper left corner of the cheque.

How to identify a CTS cheque?

You can identify a cheque as a CTS cheque when you see The printer’s name with CTS-2010 written across the left side of the cheque. But after all, you should notice and ensure these points also-

Should follow

- Ensure to use only CTS-2010 standard cheques. CTS-2010 shall be printed on the left side of the cheque.

- Write clearly and legibly and always use permanent ink pens such as a ball pen.

- Write all the details (beneficiary name, date, amount in words and figures) on the cheque using the same pen, at once and do it all yourself. It not only helps you to avoid mistakes but also prevents any misuse.

- Begin writing the amount in words close to the word “Rupees” without leaving too much space in between the words written & end with the word “only”. The amount in figures must be written close to the “?” box and put “/-” after the amount in numbers and strike through unused space in the name and amount fields to avoid any further additions.

- Sign clearly and only in the space provided.

- Alteration is permitted only in the date field. affix countersign against the altered date.

- Make sure that no cheque is removed from the cheque book without your knowledge and ensure that spoiled cheques are completely destroyed.

- Ensure that cheques are kept in a safe and locked place and never leave cheques whether signed or unsigned unattended.

- Report immediately to your bank if there are cheques missing from your cheque book or discrepancies in your bank statement and even request stop payment for the lost cheque and cheque book.

- Ensure your account has sufficient funds before you issue a cheque.

- For a canceled cheque, write “canceled” clearly across the cheque to make it unusable.

Should not follow

- Write below the MICR (Magnetic Ink Character Recognition) field of the cheque to allow the smooth clearing of your cheque. The MICR field is usually a 5/8 inch band at the bottom of the cheque.

- Sign any blank cheque or give any blank cheque as payment

- Use an erasable pen or pencil, which can be easily erased and written over, to write details on a cheque.

- Fold, pin or staple written cheques. If the cheque is folded, the clarity of the wording, which falls across the “folded” lines, may be affected.

- Alter/ amend/ erase content on the face of the cheque.

Who can participate in the Cheque truncation system?

There can be four types of participants such as-

- Member banks of the Clearing House.

- Sub Member banks who will participate through members

- Indirect members can participate in the submission of data and images through a Member bank but will maintain a separate settlement account.

- Banks are not present in the Clearing House but have a presence in other cities when Grid is introduced (to be finalized in consultation with RBI). They can participate through sub-membership or indirect membership routes.

Are there any image specifications for the cheque truncation system?

The image specifications are the same as those published by RBI. There are three images as per the following standards

| Sr. No. | Image Type | Minimum DPI | Format | Compression |

| 1 | Front Gray Scale | 100 DPI | JFIF | JPEG |

| 2 | Front Black & White | 200 DPI | TIFF | CCITT G4 |

| 3 | Reverse Black & White | 200 DPI | TIFF | CCITT G4 |

What is the CTS cheque-clearing time?

CTS cheque clearing time is Settlement on T+1 Basis i.e. customer can get funds on the Next working day, subject to bank policies.

Other Faqs on CTS (cheque truncation system)

Only CTS-2010 standards-compliant instruments can be presented for clearing through CTS.

Banks have been advised to issue only CTS 2010 standard-compliant cheques from September 30, 2012. Earlier, there were septate clearing sessions for non-CTS cheques. However, they were discontinued effective December 31, 2018. As of now, non-CTS cheques cannot be presented in CTS. The bank has been advised to withdraw the non-CTS cheques from the customers. However, non-CTS cheques remain to be valid as a negotiable instrument.

Under the One Nation, One Grid project, three CTS grids explained above are to be merged to create a single grid for the nation. A single grid shall benefit customers with the faster realization of outstation cheques. It shall also benefit banks with easier fund management, streamlining of infrastructure, and overall efficiency improvements.

Under CTS, cheque processing locations in India are consolidated into three grids in Chennai, Mumbai, and New Delhi.

CTS stands for -Cheque Truncation System in the banking sector.

Cheque Truncation System was started in the following states as follows:

New Delhi: From 1st February 2008.

Chennai: From 24th September 2011.

Mumbai: From 27th April 2013.

CTS has now been adopted throughout the country.

CTS-This is based on a cheque truncation or online image-based cheque clearing system where cheque images

MICR-magnetic ink character recognition data are captured at the collecting bank branch and transmitted electronically.

RBI will manage the Clearing House, carry out the settlement of clearing transactions that NPCI processes and look into all policy-related matters.

RBI has mandated NPCI to operationalize CTS. NPCI will act as a Cheque Processing Centre (CPC) and will process electronic cheques and images received from member banks.

Grid Clearing is an arrangement that allows banks to present/receive cheques from/to multiple cities in a Single Clearing House through a service branch in one city.

Speed Clearing is an arrangement to clear intercity non-at-par items.

An Accountant, GSTP, GST blogger, Website Creator, SEO Builder & Co-founder of the website https://gstportalindia.in for the help of GST Taxpayers of India. Having a perfect accounting experience of more than 10 years in a Private Ltd Company.