Types of cheques-There are different types of cheques that can be explored in India on the basis of the relation between the cheque drawer, drawee, and the payee. Today in this post, we are going to describe all types of cheques. And this post will help to understand the different names and types of cheques in different types of situations.

First of all, You should know what is cheque if you are a beginner or student to understand more.

Contents of this post

What is a cheque?

A “cheque” is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand and it includes the electronic image of a truncated cheque and a cheque in the electronic form.

For the explanation of the cheque according to the negotiable instrument act.

(a) “a cheque in the electronic form” means a cheque drawn in electronic form by using any computer resource and signed in a secure system with a digital signature (with or without biometrics signature) and asymmetric crypto system or with an electronic signature, as the case may be;

(b) “a truncated cheque” means a cheque that is truncated during the course of a clearing cycle, either by the clearing house or by the bank whether paying or receiving payment, immediately on the generation of an electronic image for transmission, substituting the further physical movement of the cheque in writing.

In simple words, A cheque is a type of negotiable instrument. You will need a bank account, either a savings or a current account, to write a cheque in your own name or in the name of someone else, instructing the bank to pay the specified amount to the person mentioned on the cheque.

How many types of cheques can be seen?

These are the types of cheques that can be seen according to the negotiable instrument act-

A Blank cheque is a cheque which is not filled means. blank cheque may or may not have a date and payee name. It can be made A/c Payee. A cheque can be signed without a mentioned name and also can define the amount limit. Overall it is very risky to give a black cheque.

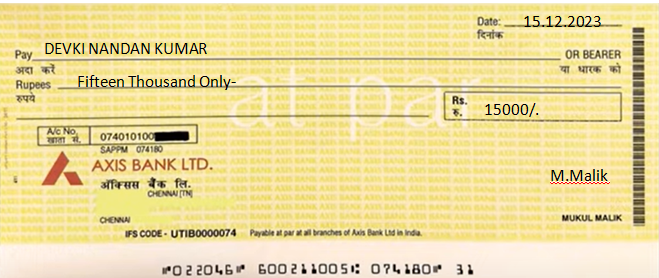

A bearer cheque is one in which the payment is made to the person bearing or carrying the cheque. These cheques are transferable by delivery, that is, if you are carrying the cheque to the bank, you can be issued the payment. The banks need no other authorisation from the issuer to be allowed to make the payment.

How can you identify a bearer cheque? You know it is a bearer cheque when you see the words ‘or bearer’ printed on them.

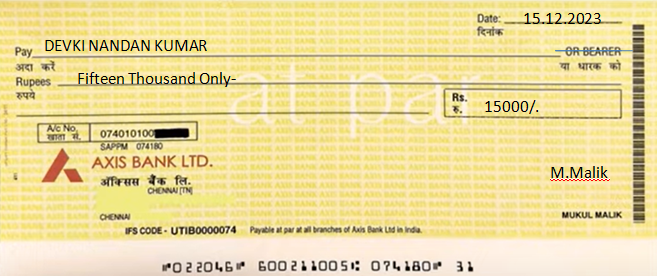

In these cheques, the words ‘or bearer’ is cancelled. Such cheques can only be issued to the person whose name is mentioned on the cheque, and the bank will do its background check to authenticate the cheque bearer’s identity before releasing the payment.

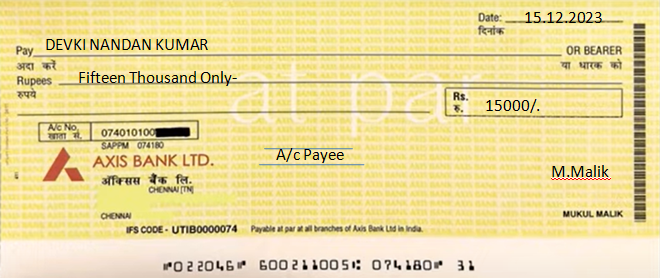

You may have observed cheques with two sloping parallel lines with the words ‘a/c payee’ written on the top left. That is a crossed cheque. The lines ensure that irrespective of who presents the cheque, the payment will only be made to the individual whose name is written on the cheque, in other words, the a/c payee along with his/her account number. These cheques are relatively safe because they can be encashed only at the drawee’s bank.

An open cheque is basically an uncrossed cheque. This cheque can be encashed at any bank, and the payment can be made to the person bearing the cheque. This cheque is transferable from the original payee (the original recipient of the payment) to another payee too. The issuer needs to put his signature on both the front and back of the cheque.

These types of cheques bear a later date of being encashed. Even if the bearer presents this cheque to the bank immediately after getting it, the bank will only process the payment on the date mentioned in the cheque. This cheque stands valid past the mentioned date, but not before.

A cancelled cheque is a cheque which has been crossed with two lines and the word “cancelled” is written across. It’s proof that the individual maintains an account with the bank. Except for this, you do not need to sign or write anything on the cheque.

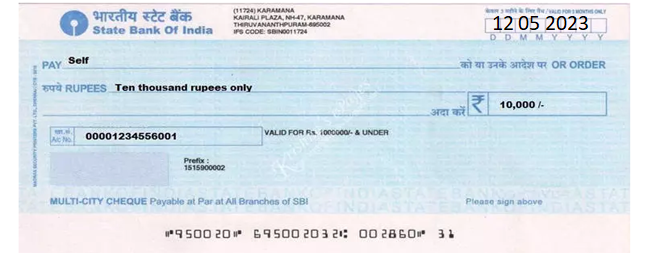

You can identify self-cheques by the word ‘self’ written in the drawee column. Self-cheques can only be drawn at the issuer’s bank.

11. Traveller’s Cheque

Foreigners on vacations carry traveller’s cheques instead of carrying hard cash, which can be cumbersome. These cheques are issued to them by one bank and can be encashed in the form of currency at a bank located in another location or country. Traveller’s cheques do not expire and can be used for future trips.

A bank is the issuer of these types of cheques. The bank issues these cheques on behalf of an account holder to make a remittance to another person in the same city. Here the specified amount is debited from the account of the customer, and then, the cheque is issued by the bank. This is the reason banker’s cheques are called non-negotiable instruments as there is no room for banks to dishonour these cheques. They are valid for three months. They can be revalidated provided specific conditions are met.

13. Normal Value Cheque

A cheque which has a value of less than 100000 Rs.

14. High-Value Cheque

A cheque which has a value greater than 100000 Rs.

15. Gift cheque

Cheques given as gifts to loved ones are called gift cheques. And the range of gift cheques can be 100 and up to 10000.

16. At par cheque

A cheque is acceptable at all branches of the concerned bank across the country. And the special thing is that while clearing it in outside branches, there is no additional charge (no additional charges).

17. Local Cheque

If the cheque of Delhi is cleared in Delhi itself, then it is called a local check. Like if I gave you a cheque in your name, then you will have to go to the relevant branch of the city with that cheque, if you take it out of the city and get it cleared, then you will be charged separately (fixed banking charges).

18. Outstation Cheque

If the local cheque is cleared by taking it out of the city, then that cheque will be called an outstation cheque for which the bank charges fixed charges.

An Accountant, GSTP, GST blogger, Website Creator, SEO Builder & Co-founder of the website https://gstportalindia.in for the help of GST Taxpayers of India. Having a perfect accounting experience of more than 10 years in a Private Ltd Company.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the ...

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.